The methods previously used in Russia to keep records of tax collectors—based on a payment booklet and the complex written reporting inseparable from it—proved in practice to be inconvenient, especially in areas with a semi-literate and illiterate population. Settlements in such areas were in most cases made “from memory” and “on trust,” while the payment booklets often remained unused and were even destroyed. In such cases, after paying monetary dues, the taxpayer received no reliable token confirming payment of the levies. Confusion often arose in the accounts, and oversight of the collectors’ own activities was hindered.

In view of this, the former justice of the peace mediator of Podolia Governorate, M.A. Skibinsky, proposed introducing for illiterate people a stamp-based system of tax administration that would eliminate arithmetic entries and be understandable to everyone. He justified his proposal by noting that the rural population had long been accustomed to settling accounts with landowners for the use of land by means of so-called “chits,” which had sometimes existed for decades and even centuries. In settlements between taxpayers and the collector, Skibinsky replaced handwritten chits with printed stamps.

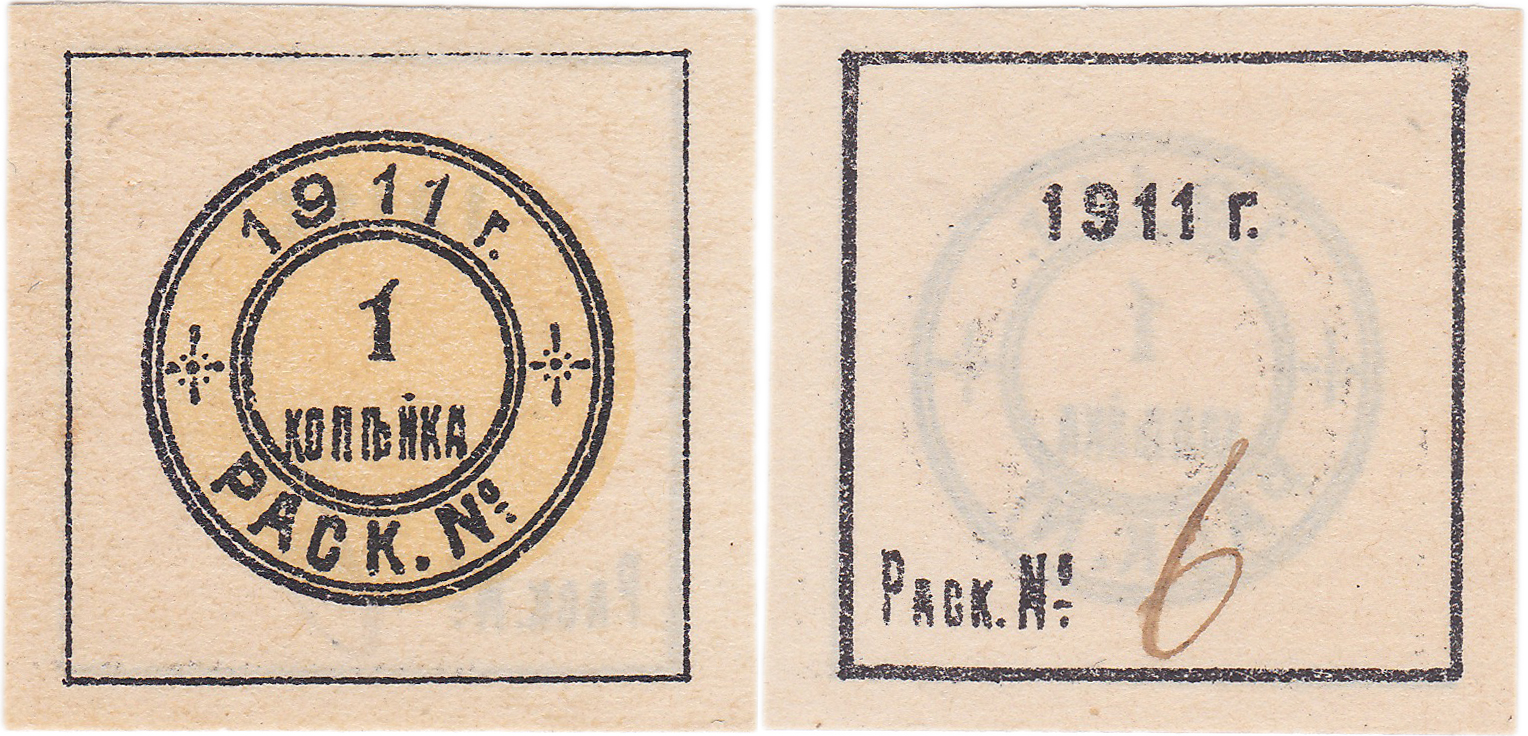

In the design of the stamps, to make them understandable to illiterate people, all the signs of monetary value long familiar to peasants were combined: stamps depicting coins worth less than one ruble were given a round shape, and the rest a quadrangular one. The coloring of the stamps matched the color of the monetary token depicted by the stamp: the one-ruble stamp was yellow, the three-ruble stamp green, the five-ruble stamp blue, the ten-ruble stamp red; silver coins were indicated in gray, copper in brown. Also, to distinguish the number of rubles and kopeks on the stamps, the corresponding number of small sticks was printed.

To control collectors on the one hand and protect the interests of taxpayers on the other, each stamp was given a personal attribution by indicating on the reverse side the number of the household head to whom it belonged. All stamps of one taxpayer were combined on a single sheet intended only for that person and secured with separate numbering. Next to the stamps on the same sheet were indicated the taxpayer’s first name, patronymic, and surname, all taxable items belonging to him according to his household register, and the levies due from him. Thus, a personal tax sheet was produced, grouping all tax demands предъявed to the taxpayer, all grounds for these demands, documentary tokens (stamps) protecting the taxpayer from multiple collection of the same levies, and all personal accounts between the taxpayer and the tax collector. The sheets of all taxpayers under the collector’s authority were bound into a cord-bound so-called “control book,” which was kept by the collector.

Tax stamps were used in collecting direct taxes from persons of the tax-paying estate living in rural areas. Initially, as an experiment, they were introduced in certain rural communities of Podolia Governorate (Ukraine), which confirmed the convenience of their use.

In practice, tax stamps began to be used starting in 1893. They were introduced in 44 uyezds of 21 governorates and in the Turkestan Region. The benefit of introducing tax stamps was recognized at congresses of tax inspectors of the Turkestan Region and Olonets Governorate, as well as by a number of gubernial and uyezd institutions for peasant affairs and by tax inspectors of many uyezds.